District Trendline, previously known as Teacher Trendline, provides actionable research to improve district personnel policies that will strengthen the teacher workforce. Want evidence-based guidance on policies and practices that will enhance your ability to recruit, develop, and retain great teachers delivered right to your inbox each month? Subscribe here.

Teacher salaries are always in the news, but in the last few months we’ve noticed that housing affordability for teachers is in the spotlight, with many school districts exploring ways to support teachers’ ability to rent or purchase homes.

San Francisco is putting in place an idea for affordable housing in a city known for the highest rents in the nation. Indianapolis, and even smaller districts, have all taken steps to ensure teachers have access to affordable housing through various community and developer partnerships.

This month, we assess the ability of teachers to: 1) rent an apartment, 2) save for a down payment, and 3) make a monthly house payment. We use salary data from our

Teacher Contract Database and couple it with rental and housing data from Zillow, a real estate website and marketplace that tracks housing and rental prices, and the US Census Bureau.

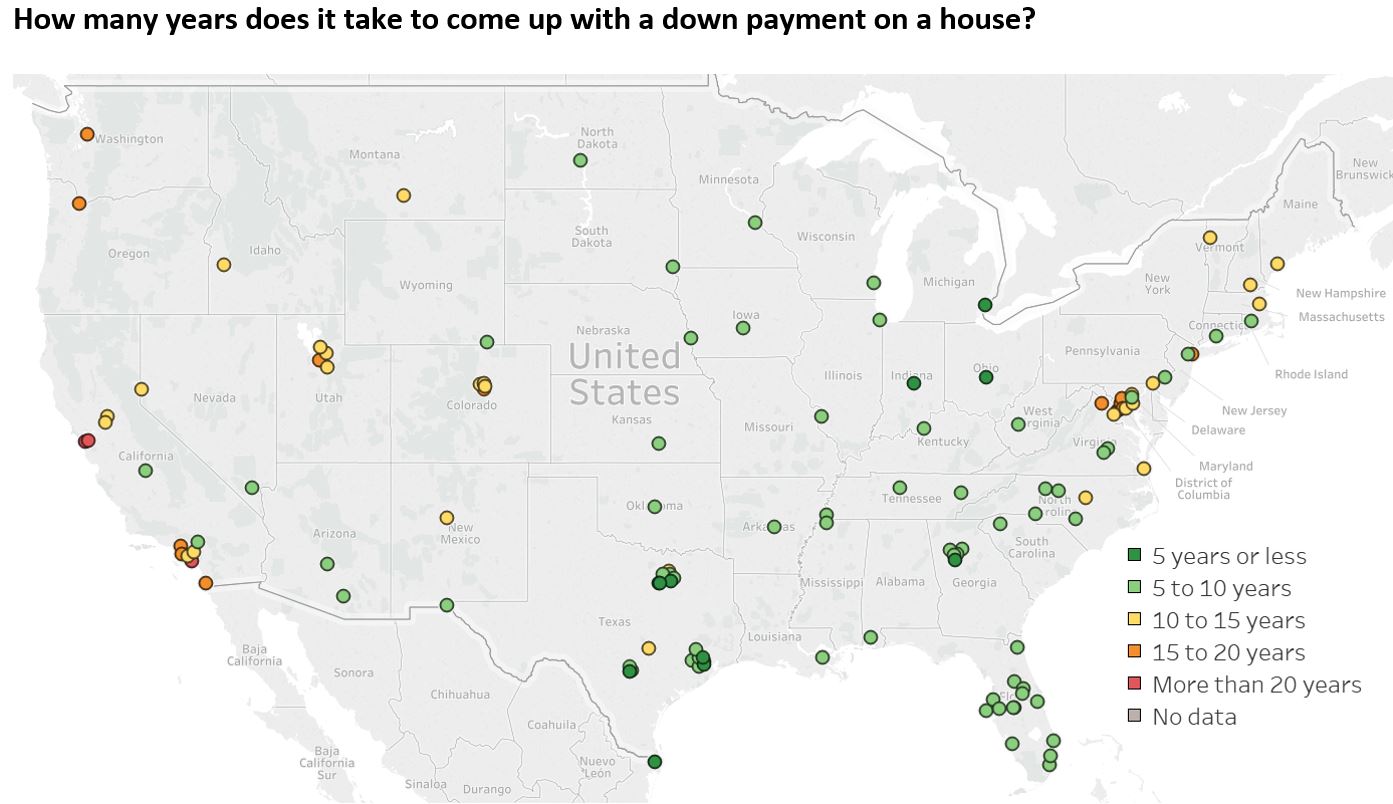

You can view an interactive map of this data

here.

Methodology

Here are the parameters we applied to conduct this exercise. We consider the 100 largest districts in the country and the largest district in each state, if not already represented in the set of 100, for a total of 124 school districts.

- We primarily focus on what a single teacher can afford, but we do briefly consider how the calculation of housing affordability changes for two-income earners.

- To estimate the cost of renting a one-bedroom apartment, we opted to use data on the median apartment rent from Zillow.[1] While the Census Bureau collects data on median rents through the American Community Survey (ACS), the Zillow data appear more representative of the rental market teachers would be facing in large cities. For example, the median rent in New York City according to ACS data is $1,202, but Zillow cites what appears to be a more realistic rent ($2,351).

- For home purchases, we use ACS data to determine the cost of the median-priced house in a district.

- For the monthly cost of owning a home, we base our calculations on the median homeowner costs in the school district using ACS data. These data include monthly mortgage payments, utilities, real estate taxes, and insurance.

Assumptions

It was necessary to make several assumptions to arrive at the relative difficulty of renting or owning a home in these 124 districts.

- Housing costs should be no more than 30 percent of a teacher’s income, a widely accepted real estate industry rule of thumb. Further, the Department of Housing and Urban Development considers families who pay more than 30 percent of their income for housing as “cost burdened,” meaning they may have difficulty affording other basic needs.

- We estimate that teachers could reasonably save 10 percent of their salaries per year towards a down payment—though we acknowledge that the definition of a reasonable amount to save for a home is certainly dependent on student loans, a teacher’s family obligations, and the local cost of living.

- Teachers, like anyone who is buying a home, typically aspire to a 20 percent down payment; anything less and home buyers must pay the additional cost of mortgage insurance. While 20 percent is the typical rule of thumb, many home purchasers make smaller down payments, as the median down payment is only 6 percent of a home’s value.[2] A lower down payment is one of many compromises that many individuals may be forced to make in order to get into a home, even though it may substantially raise the monthly cost of owning a home.

While each of these assumptions is debatable, we consider them reasonable for this exercise and in the context of the expectations of professional adults. We do fully acknowledge the many compromises not just teachers have to make to put a roof over their heads. Compromises are routinely made to secure housing—both rentals and ownership— not just in lowering the amount of down payment, but also by agreeing to living arrangements which may not be ideal such as living with parents, having roommates, or commuting longer distances to work.

Renting an apartment

We first examine if a new teacher at a starting salary in each district can afford to rent a one-bedroom apartment. In 2016-2017, starting salaries for a new teacher with a Bachelor’s degree ranged from a low of $33,829 in

Jordan School District (UT) to a high $61,750 in Corona-Norco Unified School District (CA). The average starting salary in our 124 large districts is $43,806.

In nearly three quarters (72 percent) of the districts for which there were local rental pricing data

[3], new teachers can afford to rent a one-bedroom apartment.[4]

But, put another way, new teachers cannot afford to rent a one-bedroom apartment in more than one out of four school districts.

[5]

Not surprisingly, the districts where one-bedroom rent is least affordable (shown in blue on the map below) are concentrated in or near the large cities, with San Francisco, New York City, and the District of Columbia being the least affordable for new teachers.

Rent is considered affordable when the median rent of a one bedroom apartment is less than 30 percent of a teacher’s starting salary. For further details, visit our interactive map.

Because many new teachers may be willing or even eager to live with roommates for a couple of years, we also explored if the third year salary would be sufficient. Unfortunately, teacher salaries tend to increase quite slowly, particularly in the first five years (see

Smart Money for more information). Using a sample of 10 districts located in the most expensive housing markets for teachers, we examined if teachers with three years of experience find housing significantly more affordable than first year teachers. On average, third year teachers would need to spend three percent less of their income on renting than first year teachers, but in all ten cases third year teachers would still be spending more than 30 percent of their income on rent.

Saving up for a down payment on a home

As anyone who has bought a home knows, a sizeable down payment makes it easier to get a loan and lowers the cost of a monthly mortgage. We examine how long it takes for a teacher to save a 20 percent down payment on a home that is listed at the median value in the school district, assuming a 10 percent annual savings contribution.

[6]

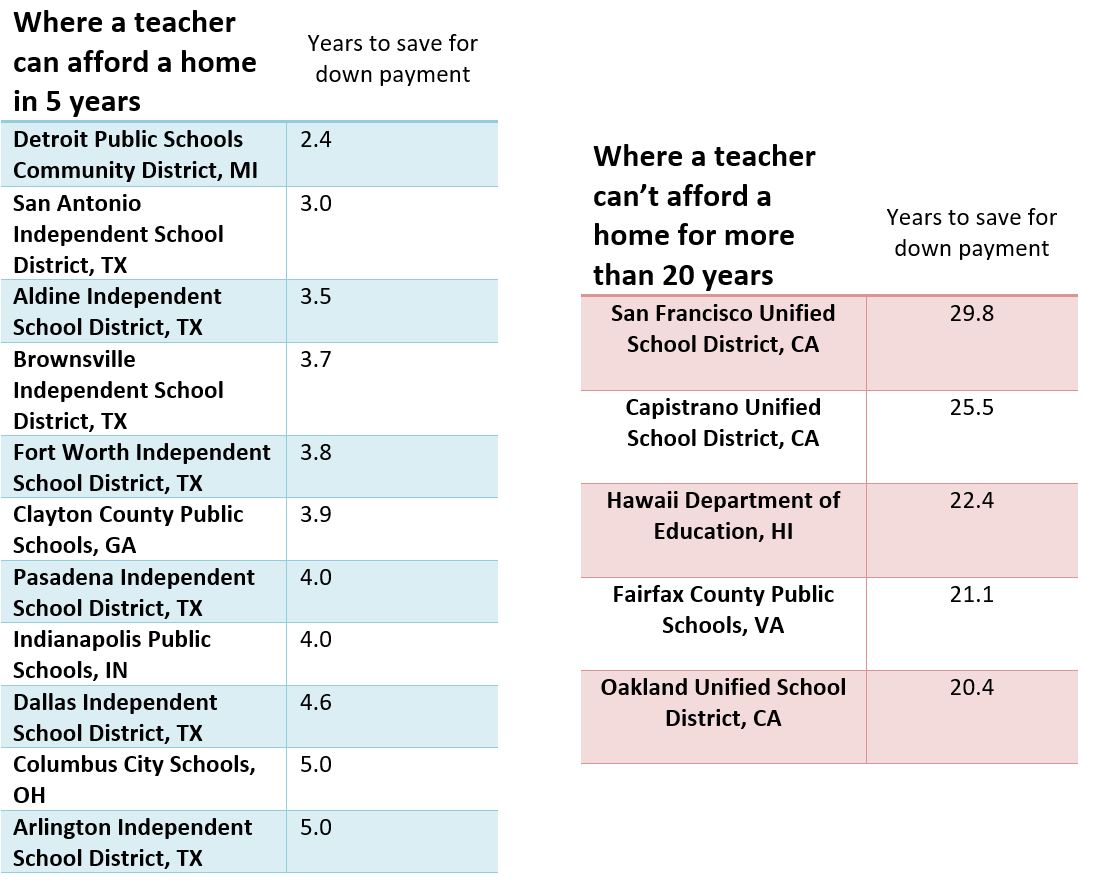

On average, across 124 large school districts, we estimate that it would take a teacher ten years of saving ten percent of their starting salary to save enough for a 20 percent down payment on the median priced home in her district.

The average masks a significant variance among districts. Assuming a 10 percent annual savings rate, it’s possible to save enough for a down payment in a little over 2 years in some districts while in others it takes as long as almost 30 years. How does this compare to non-teachers? In the majority of districts (63 percent), teachers are able to save a down payment towards a house in ten years, which is about the same pace as their non-teaching peers, given that the median age of first-time home buyers is 32 years old.

[7]

There are 11 school districts where a teacher can save up for a down payment in five years or less, seven of which are in a single state: Texas. In contrast, there are five districts where teachers would have to save for more than 20 years to save enough for a down payment, three of which are located in California.

The West and the Northeast are the least affordable areas for teachers to buy a house. Almost all of the districts in the Midwest and the South pay teachers enough to save for a down payment within 10 years.

The number of years it takes, assuming a teacher saves the equivalent of 10 percent of their first year salary each year, to put a 20 percent down payment on the median priced home in that school district. For further details, visit our interactive map.

In some places, purchasing a home may be out of reach even towards the end of a teaching career. There are 50 districts in our sample where teachers would have to save more than 10 percent a year to come up with a 20 percent down payment within five years even when making the maximum salary available. In order to reach the maximum salary, teachers usually need to have advanced degrees and, on average, 25 years of experience.

While a 20 percent down payment may be a prudent choice, many banks make it possible to buy a home with a lower amount. The average down payment for first time home buyers is six percent.

[8] With this lower down payment benchmark, a housing purchase is in reach of most early career teachers within five years, instead of ten. Of course there is a big trade off: a higher monthly house payment. There are only 15 districts where a single teacher could not afford to buy a house after five years if only paying a 6 percent down payment.

The majority of home buyers are married couples, most earning two incomes, cutting in half the time it takes to come up with a down payment.

[9] Buying a house in most of the districts in our sample (62 percent) is within reach of two married teachers within 5 years, even if they start at the bottom of the salary schedule, as opposed to the 20 percent of districts where this is possible on a single starting teacher’s salary. There remain four unaffordable districts (San Francisco Unified School District, Oakland Unified School District, Capistrano Unified School District (CA), and the Hawaii Department of Education) where buying a house in five years is a financial challenge even for two teachers earning the districts’ top salaries.

Affording the monthly housing bill

We next looked at the monthly cost of home ownership, exploring if the median monthly payments are affordable for someone on a teacher’s salary after making a down payment on a home.

[10]

Even in places where housing is relatively affordable, teachers are likely to struggle to make these payments. For example, among the 31 districts with the least expensive monthly housing costs are 16 districts where a teacher with five years of experience cannot comfortably afford monthly housing costs. These districts are generally located in the South and Midwest, including places like

Oklahoma City Public Schools, El Paso ISD, and Omaha Public Schools.

It is only a small fraction of the districts (20 percent) where a teacher with five years of experience can comfortably afford the monthly costs associated with buying a median-priced home, even assuming that the teacher has earned a Master’s degree and the boost in salary that generally comes with it.

San Antonio ISD, Baltimore City Public Schools, and the School District of Philadelphia are the most affordable for teachers. In these districts, teachers with five years of experience and a Master’s degree can put less than 25 percent of their income towards monthly house payments.

In about 45 percent of districts, the monthly bill is a real stretch, falling within 30 to 40 percent of their income. In 35 districts, over one out of four districts in the sample, teachers need to spend more than 40 percent of their income on the monthly house payment.

[11]

Paying the average monthly housing bill is consistently unaffordable in eight districts. In those districts, a single teacher will

never be able to dedicate less than 30 percent of their income to homeowner costs, even at the top of the salary schedule.

Homeowner costs are considered affordable when the median homeowner costs are less than 30 percent of a teacher’s salary (assuming the teacher has earned a Master’s degree and has five years of experience). For further details, visit our interactive map.

As you might expect, teacher couples fare better against the total cost of homeownership. After five years each of teaching, the salaries of two teacher salaries are enough to allow a couple to comfortably make a monthly housing payment in all but one district.

San Francisco Unified School District is the only district where two teachers with Master’s degrees and five years of experience cannot comfortably afford monthly homeowner costs.

Summary

Overall, we find that while renting a one-bedroom apartment is within reach for most teachers, the costs of homeownership are a stretch, particularly in the West and Northeast. Almost all of the districts in the Midwest and the South pay teachers enough to save for a down payment within 10 years.

It is the monthly housing payment where teachers are likely to struggle most. Even in districts where a home is considered affordable, most teachers would have to expend more than 30 percent of their income on housing payments.

Want to know more?

Visit the interactive map to see all the salary and housing cost details in each district or view our findings in each district here (pdf) or download the data here (Excel).

NCTQ would like to thank Dick Startz, Professor of Economics at the University of California, Santa Barbara, for reviewing this work and offering his feedback.

The Teacher Contract Database includes information on 147 school districts and 2 charter management organizations in the United States including: the 100 largest districts in the country, the largest district in each state, and the member districts of the Council of Great City Schools. The database features answers to over 100 policy questions and provides access to teacher contracts, salary schedules, and board policies in addition to relevant state laws governing teachers.

[1] To represent the median rent, NCTQ uses the average Zillow Rent Index of the Median Rent List Price for a one bedroom apartment for the county where the district is located from 2011 to 2015. If the county level data is unavailable, NCTQ uses the district’s metropolitan area. In some areas, no data were available.

[2] According to the National Association of Realtors.

[3] For 15 districts (Mobile County (AL), San Bernardino City (CA), Washoe County (NV), Cumberland County (NC), Winston-Salem/Forsyth County (NC), Bismarck (ND), Knox County (TN), Brownsville (TX), Alpine (UT), Davis (UT), Burlington (VT), Kanawha County (WV), Milwaukee (WI), Laramie County (WY)) there were no rental pricing data available.

[4] We assume the new teacher starts on the first step of the salary schedule having earned only a Bachelor’s degree.

[5] A similar analysis of ACS data yields very different results: instead of 30 districts where rentals are out of reach, there are only eight such school districts.

[6] We do not take into account any potential interest or return on investment.

[7] National Association of Realtors

[8] According to the National Association of Realtors

[9] According to the National Association of Realtors, 66 percent of recent home buyers were married couples.

[10] NCTQ uses data on the median homeowner costs from the American Community Survey which includes payment on mortgages and other property debts, real estate taxes, insurance, and utilities.

[11] In ten districts we do not have salary data for a teacher with a Master’s degree and five years of experience.

More like this

Upping the ante: The current state of teacher pay in the nation’s large school districts

As we close in on one year of the COVID-19 lockdown, we examine how resources are being used to recruit and retain effective teachers.